|

|

Calvin Cox

Partner‑VP Mortgage Banking NMLS 256450 Change Home Mortgage Office: (808) 743-1225 Fax: (303) 496‑1970 E-Mail: calvin@changemtg.com |

|

|||||||||

| If you can't see the newsletter, or would like to view it online, use this link |

| |

||||||||||||||

|

||||||||||||||

| For the week of Nov 11, 2024 --- Vol. 22, Issue 45 |

A Look Into the Markets |

All the financial markets moved sharply this week in response to election day. Let's discuss what happened and look at the week ahead. "Let's go Crazy, Let's Get Nuts" Let's Go Crazy - Prince and the Revolution. The Results This past week, Donald Trump was elected to become the 47th President of the United States. As far as the balance of power is concerned, Republicans also captured control of the Senate, and the House of Representatives is yet to be determined. This surprising sweeping victory sent shockwaves through the financial markets on Wednesday. The Reaction Interest rates had endured a horrible October, with home loan rates climbing 0.75%. Many were hopeful the increase in rates would end once election day came and went. That is not how things worked out. On Wednesday morning, interest rates opened the day sharply higher, with the 10-year Note rising nearly 20 basis points and hovering just beneath 4.50%. Traders cited several reasons for the sharp spike in rates, including future higher economic growth, higher inflation threats, fewer Fed rate cuts, and continued Federal deficits as a result of tax cuts. It is important to remember that this was the knee-jerk reaction to an already higher interest-rate trend that started back in mid-September. Stocks, which love economic growth and lower taxes, exploded to the upside with the Dow Jones closing nearly 1500 points higher to a new historic high. Bitcoin also traded to a historic high of 75,000. The U.S. dollar strengthened sharply on the notion of a stronger economic outlook and fewer Fed cuts. Debt Is still a Problem A major problem for the bond market now and in the immediate future is the accumulation of runaway debt. As of press time, our national debt is approaching nearly $36 trillion. This year alone, we will run a nearly $2 trillion deficit, the third highest in the history of our country, behind the Great Recession and the pandemic. Last Monday, we witnessed an example of the problems associated with elevated debt levels, as our Treasury Department had to offer buyers higher interest rates to purchase the $50+ billion in three-year notes offered. When auctions do not do well and higher rates are required to sell the debt, it causes interest rates to rise around the globe - and they did. 4.50% Yield resistance for the 10-year Note is now 4.50%. Hopefully this level will halt rates from moving higher. If it doesn't, rates will climb again to retest 4.70% - the highest levels of the year. Bottom line: The financial markets continue to try to price in where they see the economy, inflation, and the labor market headed next year and, as a result, what the Fed will do about it. Looking ahead Next week, Fed Officials will be out speaking and commenting on the economy and monetary policy. This will be the first time they are talking after the October Jobs report released on November 1st. Back in August, the Fed said any further cooling in the labor market would be unwelcome. One would imagine they could not be too pleased with that reading. We will also get important readings on inflation, including the important Consumer Price Index, where the Core reading actually ticked above expectations in the previous month. |

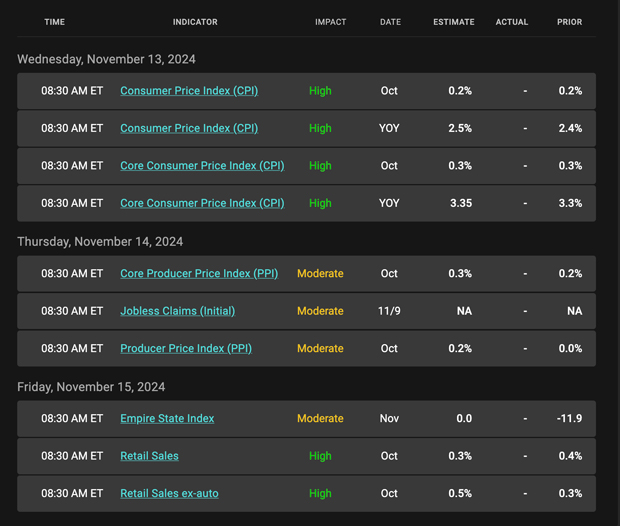

Economic Calendar |

|

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa. If you look at the right side of the chart, you can see the trend of lower prices and higher rates remains intact. Chart: Fannie Mae Mortgage Bond (Friday November 8, 2024)

Economic Calendar for the Week of November 11 - 15

|

|

|